Get a simple, easy-to-understand understanding of basic coverage car insurance. Get to know about liability, PIP, uninsured motorist coverage and remain covered.

Introduction

The first step in financial smartness that a driver can make is to understand basic coverage car insurance. Although taking auto insurance is a legal requirement in most states, a large number of individuals purchase this insurance without understanding its contents and the reasons why it is important. They simply need to be assured of insurance and the cheapest possible price.

Such a strategy may have expensive errors. One accident will put you under a medical payment, which will be fixed, and also legal complications, which will be a lot more than what minimum coverage would cover. This guide takes you through all you need to know in simple practical terms in a manner that you are able to make informed decisions without feeling overwhelmed.

The Essentials of Basic Coverage.

In its simplest form, basic coverage car insurance is the bare minimum coverage to be able to legally drive. These coverages are meant to insure other individuals with money in the event of an accident that you cause, and not your own car.

The Reasons why States need Minimum Coverage.

Auto insurance is needed in state governments to enable drivers to:

- Pay for injuries they cause

- Cover of damage to other property or cars

- Lower unpaid accident medical and legal expenses.

Although these requirements do form a safety net, they are usually only a beginning.

Essential Elements of Entry-level Car Insurance cover.

The majority of the policies developed based on basic coverage car insurance consist of a limited set of vital coverage.

Personal Liability Insurance.

The basis of any auto insurance policy is the personal liability cover. It compensates against injuries or damage you cause to other people in an accident.

There are two major categories of this coverage:

- Bodily injury liability

- Property damage liability

Bodily Injury Liability Coverage.

Bodily injury liability indemnifies:

- Medical intervention on injured passengers or drivers.

- Rehabilitation costs

- Lost wages

- Legal defense if you are sued

Coverage limits typically represent three numbers, e.g. 100/300/100.

Damage to Property Liability Insurance.

The liability of property damage includes damage to:

- Other vehicles

- Buildings

- Fences

- Guardrails

- Utility poles

When there is an accident, even with minor ones, the property damage might turn out to be costly, particularly in cases of newer cars or in cases whereby the property is a business.

Learning About Coverage Limits.

It is important to know how limits operate in order to have some idea about basic coverage car insurance.

According to Person and Per Accident Limits.

- Per person puts restrictions on the amount that is paid to one injured person.

- Accident limits coordinate the sum total of payment of all injuries separately.

You can be held personally liable to the difference between costs and these limits.

Uninsured and Underinsured Motorist Coverage.

Most states make uninsured motorist cover part of basic coverage motor insurance.

Why This Coverage Matters

Uninsured motorist insurance provides coverage upon:

- The driver to blame is uninsured.

- The coverage limits of the other driver are low.

This coverage will be useful in covering medical expenses, lost wages and even vehicle repairs.

The action of Underinsured Motorist Coverage.

The application of underinsured motorist cover is in case:

- The other motorist is insured.

- Their policy is not inclusive of your damages.

- Your limit of policy is greater than theirs.

This will make you not to be caught up with unpaid expenses.

Medical Payments and Personal Injury Protection (PIP).

Personal Injury Protection should be provided as part of basic coverage car insurance in certain states.

What PIP Covers

PIP pays for:

- Medical bills

- Rehabilitation costs

- Lost wages

- Funeral expenses

It is irrespective of the cause of the accident.

Medical Payments Coverage

Medical payments coverage is similar to PIP but more limited. It typically covers:

- Doctor visits

- Hospital stays

- Emergency care

It does not usually cover lost income or extended services.

No-Fault Insurance States Explained

Medical payments coverage is the same but less comprehensive. It typically covers:

How No-Fault Systems Work

Explanations of No-Fault Insurance States.

- Your injuries are paid by your own insurance.

- Minor injuries do not have lawsuits.

- PIP coverage is required

This system accelerates the claims but puts more emphasis on setting the right limits.

Basic Coverage exclusion.

One of the misconceptions concerning basic coverage car insurance is that it covers your own car.

Coverage Gaps to Be Aware Of

Basic policies normally do not include:

- Damage to your own car

- Theft or vandalism

- Weather-related damage

- Animal collisions

Such risks involve optional coverages.

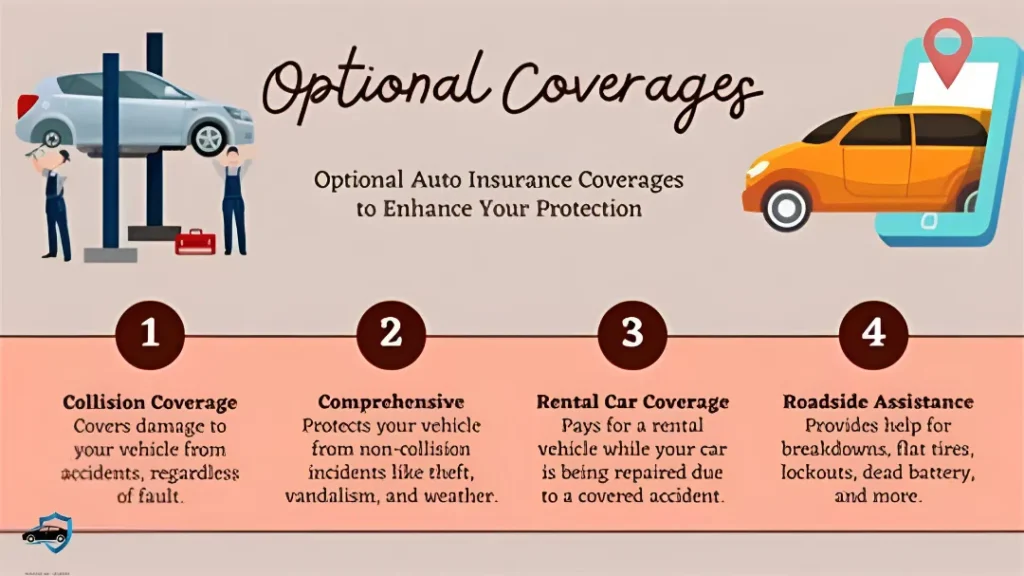

Additional optional coverages are usually added later.

Although it is not included in basic coverage of car insurance, most drivers would be going to provide additional cover as time passes.

Collision Coverage

Collision insurance is paid to fix or replace your car in the event of:

- Crashes with other cars

- Single-vehicle accidents

- Rollovers

- Hitting objects

Comprehensive Coverage

Non-collision non-accidental damages are included in comprehensive insurance and they include:

- Theft

- Fire

- Floods

- Falling objects

- Windstorms

- Animal damage

The case against Minimum coverage most of the time.

Financially, basic coverage car insurance is normally insufficient in serious accidents.

Real-World Cost Examples

- Emergency medical services may cost more than 50,000.

- Repairs of new vehicles cost above 40,000 dollars to replace.

- The court decision can be as high as six figures.

There can be minimum limits that are depleted fast.

The attitudes of Insurance Companies to Risk.

Insurance companies offer basic coverage car insurance at prices depending on the risk factors.

Key Rating Factors

- Driving history

- Accident claims

- Vehicle type

- Annual mileage

- Location

- The credit history of most states.

High-risk drivers often face higher premiums and fewer coverage options.

Risky drivers usually can have more premiums and limited options in cover.

Risky Drivers and Mandatory Filings.

SR-22 and FR-44 Certificates

These certificates confirm that you qualify in state insurance and are certified after:

- Driving uninsured

- Reckless driving

- DUI convictions

They raise the insurance rates and regain driving rights.

Selecting the Right Limits of Coverage.

Limit selection is one of the most critical choices to purchase basic coverage car insurance.

Among These are When to Raise Liability Limits.

Consider increased limits in case you:

- Own a home

- Have savings or investments

- Drive in high-traffic areas

- Transport passengers often

Increased limits are not that expensive as most individuals anticipate.

Common Myths About Basic Car Insurance

Clarification of wrong information will assist you to use basic coverage car insurance right.

- You are completely covered (you are not) with minimal coverage.

- Full coverage implies that everything is covered.

- Red cars cost more to insure

- Filing a claim is always bad

Knowledge of policy particulars is more important than guesses.

The Guide to Saving Money and Still Being Protected.

It is also possible to control expenses and enhance the basic coverage car insurance.

Smart Cost-Saving Tips

- Combine auto policies and home policies.

- Have a good driving history.

- Gradual raise of deductibles.

- Enquire on safe-driver discounts.

- Review coverage annually

What is the Process of Making a Claim.

Part of standard coverage car insurance is claims dealing that is neglected.

Typical Claim Process

- Report the accident

- Submit documentation

- Work with an adjuster

- Accept compensation or corrections.

- Make payment deductible (where necessary).

The quickness of communication increases the speed of resolution.

The Importance of Knowing What You Are Getting.

Knowing the basics of coverage car insurance prior to having an accident is in control.

It helps you:

- Avoid unexpected expenses

- Reduce legal risk

- Protect long-term assets

- Confident coverage decisions Make.

Insurance is the best taken deliberately and not in a hurry.

Final Thoughts

Auto insurance could not be confusing and stressful. With the knowledge of the simple coverage car insurance, you are certain of having clarity, confidence and financial security. Minimal coverage can be legal but informed decisions will safeguard your future.

Spare some time and look through your policy, learn your limits and change your coverage as your life evolves. Some bit of knowledge today can save a lot of trouble tomorrow.

FAQs RELATED TO BASICS COVERAGE CAR INSURANCE

1 . What is basic coverage car insurance?

Basic coverage is normally the minimum insurance which is stipulated by law. It generally provides coverage on liability of damages you do to others and property.

2 .Does basic coverage cover my own car?

No. Basic coverage does not normally cover the repair of my own car following an accident. To that you would require collision or comprehensive coverage.

3 . With basic car insurance, who is covered?

Basic car insurance will cover other motorists, passengers and property in case you cause a road accident. It also serves to insure you against a huge legal, or medical bill.

4 . Is full coverage more expensive or less expensive than basic coverage?

Yes. Simple coverage is normally cheaper since it does not provide a lot of protection to full coverage that covers collision and comprehensive insurances.

5 . Is there an option to upgrade the basic coverage in the future?

Yes. In most cases, you can always add additional coverage, e.g. collision or comprehensive, at any point, as per the regulation of your insurer.