When to Drop Full Coverage on Auto insurance made simple. Learn 7 smart signs to cut costs, avoid overpaying, and choose the right coverage for your car with confidence.

Introduction:

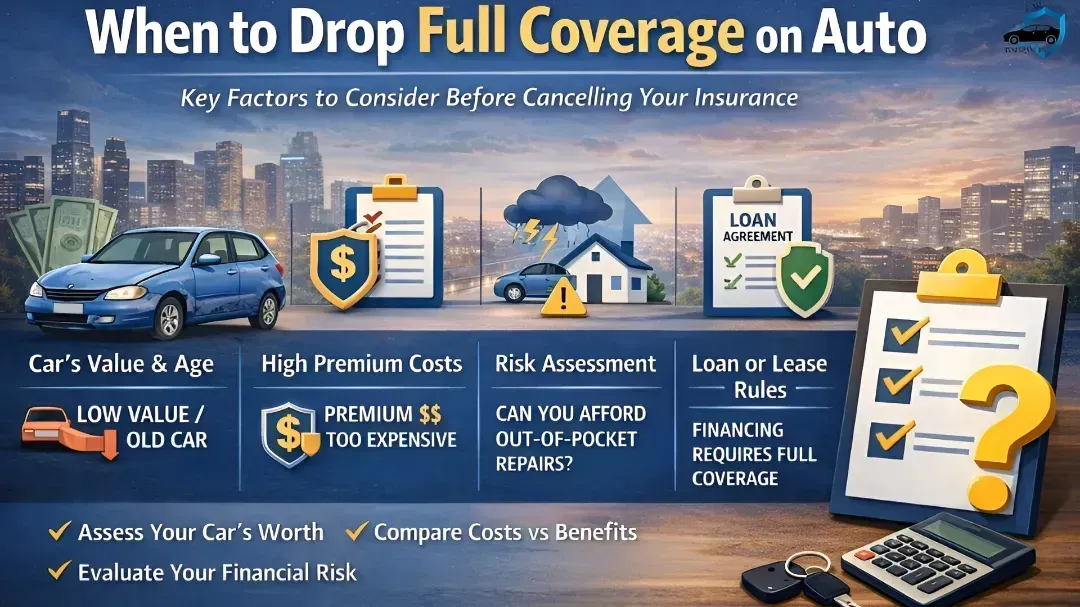

Deciding When to Drop Full Coverage on Auto is a key decision that many drivers face as their cars age. Full-coverage insurance, which typically includes liability, collision and comprehensive insurance, provides the most complete level of protection for your vehicle, but it also costs quite a bit more than just liability coverage. If you have a newer car, then full coverage makes sense since it protects you against costly repairs due to an accident, theft or natural disaster. But, as your car’s value depreciates and the market value decreases you may find that high premiums don’t provide many actual benefits from the policy.

Many drivers don’t realize that When to Drop Full Coverage on Auto on an old car, you could end up paying more than it’s worth. Knowing details such as your car’s current market value, deductible, how often you drive and whether you can afford out-of-pocket costs is important to making an informed decision. Further, if your car is financed or leased, you may also need full coverage by lender mandate which means the choice to drop coverage also depends on contractual commitments.

This ultimate guide will explain to you in detail when to drop full coverage on auto, helping you clearly understand when to drop full coverage on auto based on your car’s value, insurance costs, and personal financial situation. Knowing when to drop full coverage on auto is not always obvious, especially for drivers who want to save money without exposing themselves to unnecessary financial risk. That is why this guide focuses specifically on when to drop full coverage on auto by breaking down real-world scenarios, step-by-step decision-making methods, and expert-backed strategies. If you have ever questioned when to drop full coverage on auto for an older vehicle, a low-value car, or a vehicle that is rarely driven, this guide is designed to give you clarity.

Understanding when to drop full coverage on auto also requires evaluating financial implications, risk tolerance, deductible costs, and long-term savings potential. This guide explores when to drop full coverage on auto through practical examples, insurance comparisons, and realistic risk analysis so you can confidently determine whether full coverage still makes sense. Whether your goal is to save money, optimize your insurance policy, or simply learn when to drop full coverage on auto without making costly mistakes, this resource provides straightforward guidance you can trust. By the end, you will fully understand when to drop full coverage on auto, gain the tools to judge your insurance needs with confidence, reduce unnecessary costs, and strike the right balance between savings and protection for your vehicle.

What Full Coverage Includes

Liability, collision and comprehensive coverage make up full coverage. Each serves a distinct purpose:

Liability Insurance:

Mandatory in most states, liability insurance covers injuries and property damage that you cause to other people.

Collision Coverage:

When you damage your car in an accident, regardless of fault. Typically comes with a deductible, and is necessary for new or financed vehicles.

All Comperhensive:

all non-collision damages covered including theft, vandalism or disasters.

Additional coverages occasionally included with full coverage policies include:

- Uninsured/Underinsured Motorist: Covers you when the other driver is not well-insured.

- Personal Injury Protection (PIP) or MedPay: Covers medical costs for you and your passengers.

- Gap Insurance – This coverage protects the policyholder from a difference between the loan balance and actual value of the vehicle if totally lost.

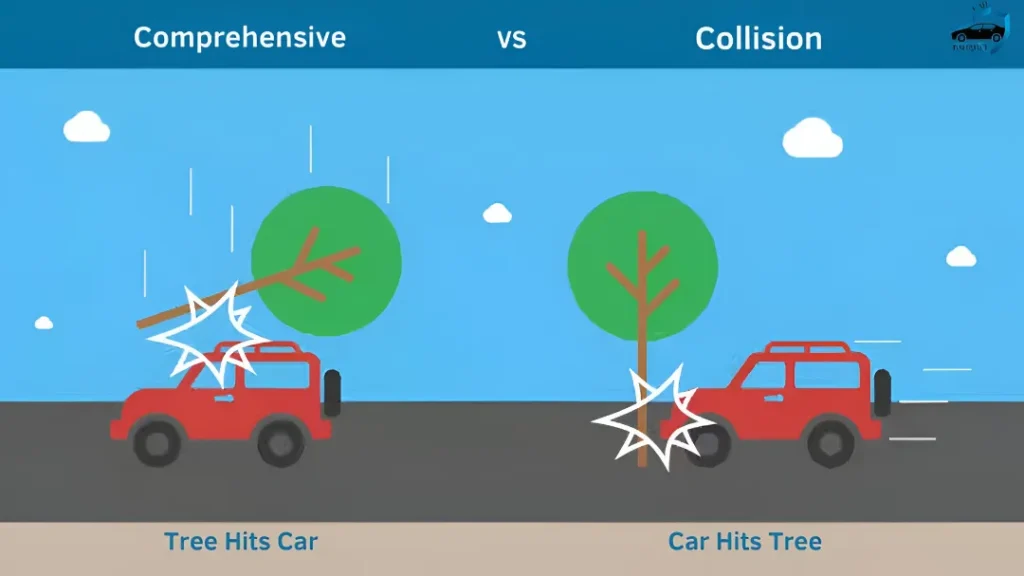

Differences Between Comprehensive and Collision

And even though a lot of these two terms gets confused… it’s really important to understand the difference between them:

Type of coverage comparison

Collision

Damage from an accident with another car or object

Optional (If your car is financed, you will likely be required to get collision coverage)

$100-$2,000

Comprehensive

Non-collision incidents (theft, fire, weather)

Optional

$100-$1,000

Understanding the difference is helpful if you’re thinking of getting rid of full coverage in part, like by keeping comprehensive while ditching collision.

When it makes sense When to Drop Full Coverage on Auto drivers.

Full coverage can be expensive. Several drivers wonder if the coverage is worth keeping on older cars, vehicles with little value or ones that see infrequent use. The ruling is based on three main factors:

Vehicle Age and Depreciation

Cars depreciate a lot, especially during the first couple of years. According to standard depreciation rates:

- Year 1: 20-30% loss

- Year 2: 15-20%

- Year 3: 10-15%

- Subsequent years: 7-12% per year

Once the value of a car plummets under what it’d cost to repair or replace it, full coverage can feel like less pay off.

Financial Considerations and Budgeting

Full coverage in the United States costs $1,500-$3,500 annually for cars of average value. If your car is of low value, the annual premium cost may be more than the payout after a total loss and becomes inefficient.

Example:

- Vehicle ACV: $5,000

- Annual full coverage premium: $1,200

- Deductible: $500

- Max payout: $4,500

In this situation, full coverage might be too expensive to keep. Directing the savings to an emergency fund or new car fund instead might be a better idea.

Risk Tolerance Assessment

If When to Drop Full Coverage on Auto, the risk of a larger financial burden falls on you rather than against the company that insures it. Consider:

- Are you able to pay for repairs or replacement yourself?

- How essential is your car to each and every day?

- Are you living in an area where risk of accidents, thefts and calamities are less?

There’s no one-size-fits-all answer, as risk tolerance differs person by person: Some people would rather have the peace of mind full coverage provides, and some would rather pay less now and self-insure smaller damages.

Factors to Consider * Key Rules and Benchmarks to Decide

Insurance professionals frequently offer rules of thumb to help make the determination about whether it is worth dropping full coverage.

10-Percent Rule for Other Than Collision Coverage

If your collision premium is more than 10% of the value of your car, it might be time to think about dropping it.

Example:

- Vehicle value: $4,000

- Annual collision premium: $450

- 10% of vehicle value: $400

If your premium exceeds 10% of the car’s value, consider dropping collision coverage.

Vehicle Value Thresholds

Experts say to consider dropping full coverage in the following circumstances:

- Old car or low book value: Under $3,000-$5,000, the insurance payout often doesn’t justify the premium.

- Depreciation trumps coverage: Little damage can be more than the car is worth.

- A 2005 pickup worth $1,200, for instance, could run you $180 a month in full-coverage premiums. There’s no reason to drop coverage and go to liability-only insurance and save money with little risk.

Loan or Lease Requirements

If the car is financed or leased, lenders will demand full coverage for as long as you owe on it. Terminating coverage early may result in breach of contract and liability.

Evaluating Your Policy: Here’s What to Do

Follow these steps to be sure you’re making an informed decision before you drop coverage:

Calculating Net Payout vs Premium

Net payment = Actual Cash Value (ACV) – (Deductible + Annual Premium)

Example 1:

- ACV: $12,000

- Deductible: $1,000

- Annual Premium: $825

Net payout = $12,000 – ($1,000 + $825) = $10,175

Example 2 (older car):

- ACV: $5,000

- Deductible: $1,000

- Premium: $825

Net payout = $5,000 – 1,825 = $3,175

The second scenario is demonstrating “the law of diminishing returns” with older cars.

Identifying Non-Essential Coverages

Some are just pure upsell, they raise premiums by selling you something that is not really essential:

- Rental reimbursement

- Roadside assistance

- Towing coverage

By stripping away non-essential coverage, you may also be able to lower premiums without losing your core protection.

Consulting Your Insurance Agent

Insurance agents can:

- Verify your car’s ACV

- Suggest alternative coverage options

- Offer quotes for liability only, or high-deductible plans

Regional Considerations and State Laws

State rules influence minimum coverage and the risk that comes with it:

State-Specific Minimum Coverage

- Florida: PIP and PDL required

- California: Liability minimums (15/30/5)

- Texas: Liability only mandatory

How Risk In Your Area Affects Your Decision

Areas with high theft, or that are prone to hail, might justify maintaining comprehensive coverage on older cars.

Country and wildlife hazards: People who live out in the country where there is a lot of wild life may want to consider adding collision coverage for accidents with animals.

Pros and Cons of Having Full Coverage vs Only Liability

Advantages of Maintaining Full Coverage

- Protects investment in newer vehicles

- Pays expensive repairs for non-collision damage

- Required for loans or leases

- Peace of mind

Benefits of Dropping Coverage

- Significant premium savings

- Allows self-insurance for low-value cars

- Frees up money for other financial needs

Alternative Coverage Options

If full coverage sounds expensive, but you want peace of mind:

Liability Only with Comprehensive

- Keeps non-collision protection

- Reduces premium significantly

- Great for high non-collision areas

High Deductible Strategies

- Increase deductible to lower premium

- Retain coverage for catastrophic events

- Needs savings account to pay for deductible

Case Studies and Real-Life Scenarios

Older and Higher Mileage Cars

- 2005 Toyota Corolla, 17,000 miles: Probably worth considering full withdrawal of coverage

- 2008 Honda Civic, had 120k on it: Liability + comprehensive may be good enough

Financed Vehicle vs Fully Owned Vehicles

Financed cars: Full coverage required

BaretikelepMyIdeas Fully owned car, assess risk tolerance and value of the car to decide.

Final Thoughts

Knowing When to Drop Full Coverage on Auto is truly a personal, financial and strategic decision. Use these strategies:

- Analyze vehicle value and depreciation

- Assess premiums vs net payout

- Review financial ability to self-insure

- Evaluate personal risk tolerance

- Consider loan or lease obligations

- Explore alternative coverage options

- Consult insurance experts

They enable you to do this whilst avoiding excessive premiums and costs, ultimately saving money (it’s all about the Benjamins after all!). Full coverage isn’t always needed, in particular for older cars or those with a low value — but having and understanding your options means you make the best choice.

FAQs Related to When to Drop Full Coverage on Auto

1 . When to Drop Full Coverage on Auto insurance on your car?

You might be a candidate When to Drop Full Coverage on Auto insurance when your car’s market value is extremely low, you’re paying more in premiums each year than the vehicle is worth and when you have enough money set aside to pay for out-of-pocket repairs or replacement if it comes to that.

2 . Does it make sense When to Drop Full Coverage on Auto on an older car?

Yes, in many situations it would be prudent When to Drop Full Coverage on Auto on an older vehicle, especially if the value of the car is below $3,000-$5,000 and you’re paying more for the insurance policy than you could ever recoup after your deductible.

3 . If the car is financed or leased, can I eliminate full coverage?

If your car is financed or leased, no, lenders generally demand that drivers have full coverage insurance. Releasing your car before the loan or lease is paid off may also be a contract violation for you.

4 . How much coverage do I need to keep When to Drop Full Coverage on Auto Insurance ?

If you do drop full coverage, you still have to remain insured with enough liability as mandated by your state’s requirements. Lots of drivers also maintain comprehensive coverage even after they’ve dropped collision, since it provides protection against theft, vandalism or weather damage.

5 . How much can I save by getting rid of full coverage?

Savings vary, but many drivers realize hundreds to thousands of dollars in yearly savings by reducing full coverage to liability-only or partial, based on their vehicle value, address and driving history.