Save money on rental car insurance with these 15 smart, practical tips. Learn how to avoid duplicate coverage, reduce unnecessary add-ons, and understand your existing benefits before you rent. Make informed, cost-effective decisions to ensure you get the right protection without overpaying.

Introduction

Car hire insurance can be a minefield as soon as you hit the rental counter. You’re fatigued from travel, and there you are asked to decide between various protection options. Each one sounds necessary. Each one adds to your cost.

You don’t want to pay for coverage that you already have. At the same time, you don’t want to incur a financial risk if something should go awry. A minor error here could become a significant cost next.

This guide breaks down rental vehicle coverage in easy-to-understand terms so that you can make the right choice every time.

Car hire insurance often causes stress as big decisions need to be made quickly. In a brief conversation, rental agents might offer extra services such as collision damage waiver, liability coverage and personal accident protection. With no previous experience, it’s natural to agree to everything so as not to rock the boat.

But not every solution is right for you. Some vehicle damage protection or theft coverage is already built into your personal auto policy, travel insurance and even your credit card. If you do not check first, you could be paying twice for the same protection.

Education on how rental protection works is key to staying in control. Rather than responding at the counter, you make selections according to what you have on hand and what you genuinely require.

The description of coverage is also problematic. Terms such as loss damage waiver, deductible and liability limits may sound technical. In reality, they are straightforward when broken down:

Vehicle damage protection provides insurance for the car you’re renting

Liability coverage covers damage or injury to others

Personal accident schemes take care of the medical expenses

Belongings owned by you are covered by personal effects insurance

When you start to see them clearly, the choice is simpler.

Cost is also a big factor. Daily add-ons can raise your total rental price by a wide margin. What seems like a modest per-day price tag can quickly accumulate over the course of a week or more. That’s why it’s worth examining your insurance policy and credit card benefits before you take the trip.

If you already have rental reimbursement or collision protection in your current coverage, you might only need a limited number of add-ons or none.

Get the best mix of cost and protection. You want enough coverage to not get slapped with major bills, but not so much that you waste money on redundant applications.

This guide describes each option, what matters and helps you select the right balance of protection without confusion.

What Is Rental Car Insurance

Rental car insurance is a form of coverage that helps financially if you encounter an issue while driving a rental vehicle.

It typically covers:

- Vehicle damage

- Theft

- Liability for damages or injuries to property

- Medical costs

- Personal belongings

These are available as add-ons through car rental companies like Dollar Rent A Car and Hertz.

Why Rental Car Insurance Matters

With no rental car insurance, you could find yourself on the hook for:

- Full repair costs

- Loss of use charges

- Administrative fees

- Third-party damages

- Just a minor accident can be thousands.

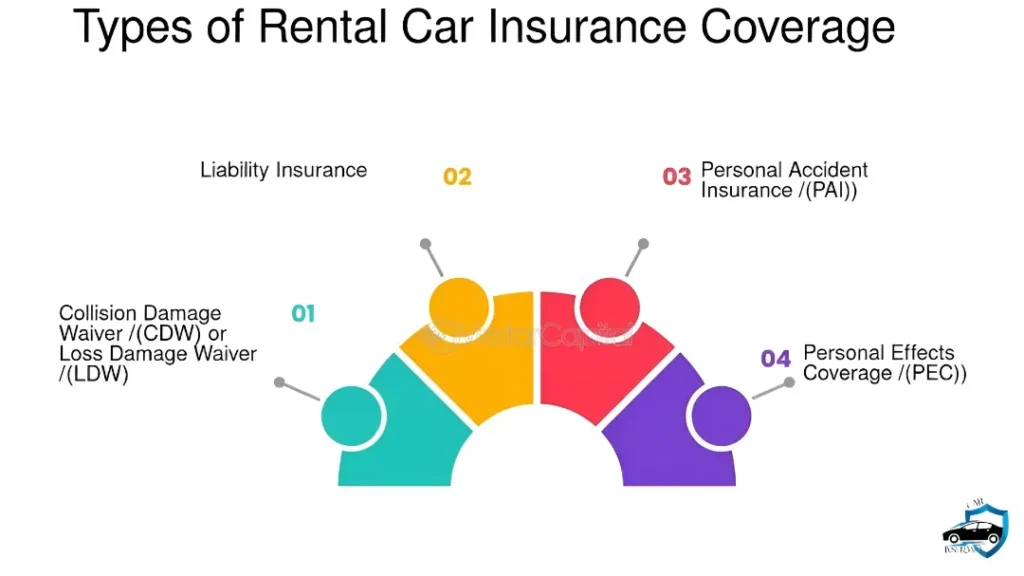

TYPES OF RENTAL CAR INSURANCE COVERAGE

Knowing the different coverage types is essential before purchasing rental car insurance.

Loss Damage Waiver (LDW)

Also known as Collision Damage Waiver (CDW).

What it covers:

- Damage to rental car

- Theft

- Vandalism

Key points:

- No deductible (in most cases)

- You don’t even have to bring your personal insurance into it

- Covers regardless of fault

Liability Insurance Supplement (LIS)

What it covers:

- Injury to others

- Damage to other vehicles/property

Typical coverage:

Up to $1,000,000 or more

When you need it:

If you have low personal liability coverage

Personal Accident Insurance (PAI)

Covers:

- Medical expenses

- Ambulance costs

- Accidental death

Helpful if your health coverage isn’t too robust.

Personal Effects Coverage (PEI)

Covers:

Theft of belongings from car

But often already covered by:

- Home insurance

- Travel insurance

Personal Protection Plan (PPP)

A bundle that includes:

- PAI

- PEI

Do you really need car rental insurance

This depends on your situation.

You MAY NOT Need It If:

- You own a personal auto insurance policy

- Your Credit Card Comes with Rental Coverage

- You already bought travel insurance

You SHOULD Consider It If:

- You don’t own a car

- Your policy carries a high deductible

- You’re traveling internationally

- You are looking for zero hassle in claims

Discover the Difference Between Rental Car Insurance & Personal Insurance

Here’s a simple comparison:

FeatureRental Car InsurancePersonal Auto InsuranceDeductibleOften noneUsually appliesClaims impactNo effectMay increase premiumCoverage speedFastSlowerCostDaily feeAlready paid

Is Rental Car Insurance Covered By Your Credit Card

Many credit cards provide rental car insurance.

Important details:

- Usually secondary coverage

- Must be paid in full with that card

- Limited coverage types

Covers:

- Damage

- Theft

Does NOT cover:

- Liability

- Medical expenses

Cost of Rental Car Insurance

Daily pricing:

Coverage TypeCost per Day

- LDW$10–$25

- LIS$7–$15

- PAI$1–$5

- PEI$2–$5

Per day can total $30–$50

How to Avoid Paying Too Much for Rental Car Insurance

You don’t have to swallow each option.

Check Your Existing Policy

Call your insurer and ask:

- Does it cover rentals?

- What’s the deductible?

Use Credit Card Benefits

Some cards include:

- Collision coverage

- Theft protection

Avoid Duplicate Coverage

Don’t pay twice for:

- Same protection

- Same risk

Compare Before Booking

Look at:

- Travel insurance providers

- Third-party rental coverage

Choose Only What You Need

Skip extras like:

- PEI if already covered

- PAI if you actually have health insurance

Rental car insurance for international trips

That’s where rental car insurance comes into play.

Key Risks Abroad

- Your home insurance likely does not cover it

- Minimum coverage may be required by local laws

- Higher repair costs

What You Should Get

- LDW

- Liability insurance

- Roadside assistance

If I opted out of rental car insurance, what Would happen?

Skipping rental car insurance can cost:

- Large repair bills

- Legal liability

- Stressful claims process

Example:

- Minor accident → $2,000 repair

- No coverage → you pay all

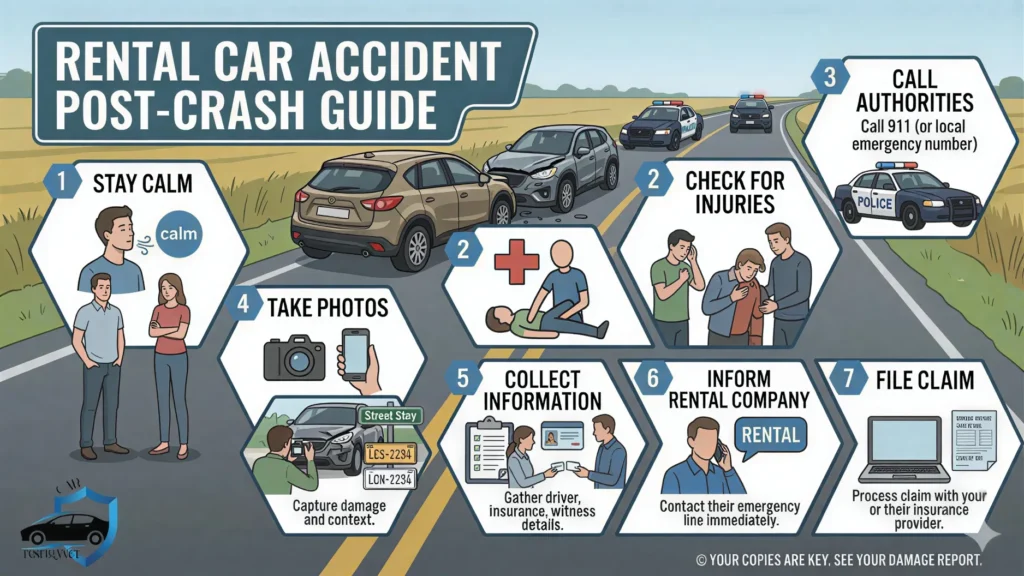

Rental Car Insurance Claim Process

If an accident happens:

Steps to Follow

- Stay calm

- Check for injuries

- Call authorities

- Take photos

- Collect information

- Inform rental company

- File claim

What to Avoid with Rental Car Insurance

Mistakes in buying rental car insurance can be expensive. Here are common traps and other reasons to remain cautious:

Saying Yes to Everything

Rental agents typically pressure customers into several insurance options at the counter. Approving everything is dangerous and may lead to avoidable waste.

Ignoring Your Existing Coverage

Your personal auto insurance or credit card might already cover rental protection. DoubledPayment The classic and Non-avoidable blunder

Not Reading Terms and Conditions

Others have certain exceptions or exclusions, such as:

- Off-road driving

- Unauthorized drivers

- Driving outside approved areas

Understanding these terms can prevent you from being open.

Forgetting Deductibles

Your policy may cover you for rental damage, but you could still be liable for a deductible. Know your limits before signing.

Assuming All Coverage Is Equal

Not every protection package is equal. Some might cover theft but not collision, or medical costs but not liability.

Overlooking International Rules

Abroad, local laws may require you to take extra coverage when renting. It is a risky assumption that your U.S. policy covers the world.

Failing to Inspect the Vehicle

Failing to document existing damage or take photos can leave you liable for scratches or dents that weren’t your fault.

Staying away from these pitfalls can save you money, stress and guarantee that you are properly protected during your rental.

What Are Deductibles in Rental Car Insurance?

Deductible = what you pay prior to insurance covering the remainder

Example:

- Damage = $1,500

- Deductible = $500

- You pay $500

LDW often removes this cost.

Rental Car Insurance: A Non-Car Owner’s Guide

If you don’t own a car:

Best Options

- Buy rental coverage

- Consider non-owner insurance

- Use credit card protection

Long-Term Rental Insurance

If you are renting for more than 30 days, long-term rental insurance is essential. You aren’t fully covered under your everyday coverage, so be sure to review your options closely.

Watch For:

- Policy limits that could limit your coverage

- Expiration of coverage for extended rentals

- Additional expenses that could build over time

Long-term rentals typically have different rules than short-term rentals. Some policies automatically cut coverage after a certain number of days, or surcharges may kick in for longer stays.

If you rent for a month or more, double-check both with the rental company and your current insurer to make sure you stay fully covered throughout the rental. This will help prevent surprise charges or coverage lapses.

Should You Purchase Insurance for Your Rental Car

Short answer: depends.

Worth It If:

- You want peace of mind

- You lack coverage

- You travel abroad

Not Worth It If:

- You’re already fully covered

- You’re making some great rewards on your credit card

Liability Risks and Rental Car Insurance

Liability is the biggest risk involved in renting a vehicle. Even a small mishap can get quite expensive without adequate liability coverage.

Without Liability Coverage

You could end up paying for:

- Medical bills for others involved

- Damage to other vehicles or property

- Legal fees if someone sues

Liability risks are often underestimated. Most renters think only about damage to the rental car itself, never considering a claim from another driver or property owner. That means tens of thousands in expenses if you end up in a major accident with no coverage.

Liability protection protects your personal assets and protects you from similar unpleasant financial obligations. Even if you have personal auto insurance, or your credit card offers some coverage, it’s a good idea to review the limits and exclusions before you do rent.

How Rental Companies Profit from Insurance

Rental companies profit from:

- High daily rates

- Fear-based selling

- Convenience

That’s why you need to know rental car insurance before you get there.

Rental agencies enhance profits by offering add-on packages that set multiple coverages together. These sales bundles typically include things you don’t need—only they are packaged as the safer choice, steering consumers toward overspending.

They have urgency at the counter. You’re often pressed for time, and decisions seem like they are time-sensitive. That makes it easier for them to upsell additional protection without allowing you time to check your current coverage.

Convenience also plays a big factor. Almost none of these are pre-existing but buying coverage on the go is less complicated than reviewing your policy or benefits on your credit card. A lot of people simply pay the extra, to avoid any hassle, even when they have similar protection elsewhere. ing.

Checklist Before Renting a Car

Before Booking

- What Does Your Auto Policy Cover for Rentals?

- Make sure you have damage or theft coverage via your credit card

- Types of coverage — Third-party and rental company

At the Counter

- Avoid paying for duplicate protection

- Inquire about limits and exclusions on coverage

- Read all terms before signing

After Renting

- Inspect the vinyl surface for scratches or dents

- Photograph or film for evidence

- Keep the rental receipts and copies of the agreement

Final Thoughts

And car hire insurance needn’t be confusing and rushed. When you know how coverage works before hitting the counter, you remain in control. You don’t make snap decisions or respond to sales pressure. Instead, you make deliberate decisions that fit your reality.

Focus on:

- Understanding coverage types

- Avoiding duplicate protection

- Paying only for what you need

“Planning before you get to the airport means no pressure at the counter, and taking better decisions.”

Car hire insurance is a topic that feels quite straightforward if broken down into sections. You don’t need all the choices that are available. You just need coverage that specifically fills in any holes in your existing policy or credit card benefits. It is cost-effective and still guards you against serious costs.

Before you go, spend a few minutes:

- Check your auto insurance policy

- Check your credit card rental perks

- Take note of your deductible and coverage limits

These steps ensure that you can make a quick decision when you’re standing at the rental desk.

Something else to remember is risk. Not having any coverage at all may save money in the short term, but can wind up costing a lot more in the event of an accident. On the flip side, purchasing every add-on without an inventory of your existing coverage can lead to unnecessary expense.

A balanced approach works best. You fill in what’s absent, ignore what you already possess.

Also, read the rental agreement. Look for:

- Exclusions (off-road use, unauthorized drivers)

- Coverage limits

- Terms for damage and claims

This will help avoid any surprises down the line if you ever need to file a claim.

Ultimately, it’s a simple objective: get coverage without overpaying. When you get the ins and outs of car damage protection, liability insurance, and how your existing policy works, you’ll make fewer stressful decisions.

Well in advance and well-informed, consume only what serves your need.

FAQs Related to Rental Car Insurance

1 . Is rental car insurance really necessary?

It can, based on what coverage you already have. If you already have personal auto insurance, credit card benefits or travel insurance, additional rental coverage may be redundant.

2 . What does car rental insurance usually cover?

Rental car insurance typically covers damage to the vehicle, theft, third-party property damage, medical expenses and personal belongings in some cases.

3 . Is Credit Card Rental Car Insurance Sufficient?

In many cases, credit card coverage is secondary — and may only cover damage or theft. It usually excludes liability or medical coverage.

4 . How do I avoid being overcharged for rental car insurance?

Check your existing insurance coverage, know what your credit-card benefits include and resist the temptation to buy handcuff-style coverage when you reach the rental counter.

5 . What does it mean if I waive rental car insurance?

Should you decline coverage and something does happen, you might pay for repair costs, liability claims, and various extra fees depending on the existing coverages that you have.